L1 Tokens

L1 Tokens

I’m not a trader. This post is just a summary of my views, not investment advice.

Something interesting has been happening to L1 token valuations: while on-chain activity continues to grow, many tokens have struggled to maintain their previous price levels. This disconnect suggests that the fundamental value proposition of these tokens may have shifted. Here’s my take on what’s going on.

ETH was money

There has been a lot of debate about whether ETH is money, but if we look at the facts, the reality is that ETH was money.

In 2017, the first major product market fit of the Ethereum chain was ICOs. It was a crazy year with a lot of exuberance, but most importantly, ICOs collected their investments in ETH. Since ETH seemed to be up only, people as well as organizations kept large parts of their investments in ETH and even used it as a primary way to value their stashes.

2020/2021 brought another wave of adoption, centered around DeFi and NFTs. Again, ETH was front and center – remember when Christie’s and Sotheby’s started showing prices in ETH?

Retrospectively, this was the highest point of ETH adoption as money. In some aspects, it had achieved the trifecta:

- Unit of Account (mostly for NFTs)

- Store of Value

- Medium of Exchange

The velocity of money equation (MV = PQ, where M is money supply, V is velocity, P is price level, and Q is quantity of goods/services) tells us that when ETH is used as money, its market capitalization (proportional to M) should be proportional to the on-chain GDP (PQ), assuming velocity remains relatively constant. In other words, as the economic activity on Ethereum grows, so should ETH’s valuation if it continues to serve as the primary medium of exchange.

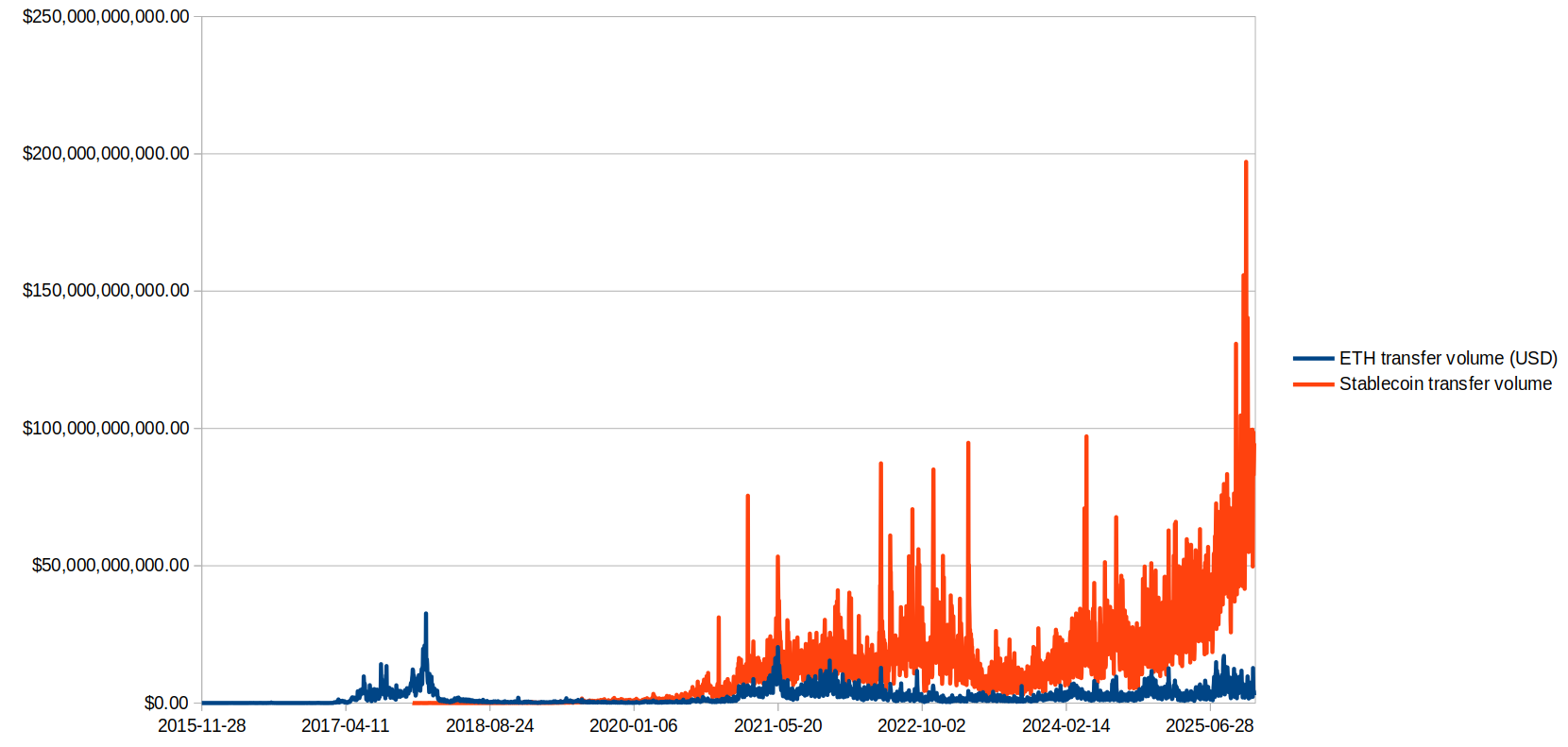

ETH was displaced by stablecoins

Since 2021, time has been less kind to ETH: NFTs lost a lot of their value, and adoption as a medium of exchange has mostly been replaced by stablecoins:

Ethereum is now rarely used as a medium of exchange or unit of account, when compared to the 2017-2021 period. This could be an explanation why appreciation of ETH seems to have stalled, while adoption is still growing.

The path forward

ETH could escape this by:

- Becoming a memetic store of value modeled after gold (and now maybe Bitcoin). However, this largely decouples it from the success of the Ethereum chain itself, and it is unclear if it will be perceived as much better than Bitcoin; the value for memetic stores of value is largely driven by brand and not technical properties

- Driving a massive campaign to re-establish ETH as money in the functions that it has lost

- Focusing on earning revenue and burning fees, aiming to have at least 10s of billions USD in revenue. This will require turning the EF into an effective R&D and BD org, as well as finding ways to continuously fund those efforts

Many L1s will face the same question. While their tokens don’t have a history of being used as money, they mostly attained their valuations by being seen as a potential replacement to Ethereum, with the implied assumption that their tokens would similarly be used as a medium of exchange. Solana did have some short success in this during the memecoin craze in early 2025, but it was even more short lived than the past drivers of Ethereum’s success.

Conclusion

The challenge facing L1 tokens is that their historical valuations were largely predicated on their use as money – specifically as a medium of exchange. The velocity of money equation suggests that when a token serves this function, its valuation will track on-chain economic activity. However, the shift to stablecoins has broken this link for most L1 tokens.

This creates a valuation problem: if tokens are no longer used as money, what drives their value? The options are: either recapture the monetary functions, pivot to a store-of-value narrative (competing with Bitcoin), or fundamentally change the value proposition by generating substantial revenue through fees and burns. The latter path requires a different kind of organization: one focused on business development and sustainable revenue generation rather than just protocol development.